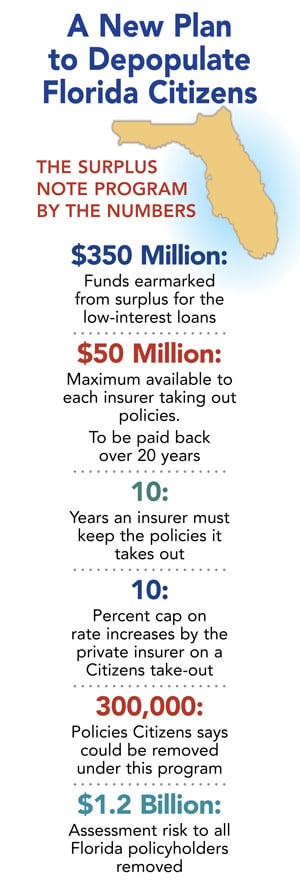

Florida Citizens Property Insurance Corp. says it plans to make up to $350 million available to private insurers willing to assume its policies.

Under a plan approved late last week by the supposed last-resort insurer that is now the state's largest property writer, low-interest 20-year loans would be made available from Citizens' surplus to qualifying "take-out companies"—those approved by the state Office of Insurance Regulation to remove policies from Citizens in order to reduce its exposure.

Barry Gilway, president and CEO of Citizens, says as many as 300,000 policies could be removed under the new loan program—possibly by the start of 2013. If so, the assessment risk over the heads of nearly all Florida policyholders would be reduced $1.2 billion (for a 1-in-100 year event), he adds.

Barry Gilway, president and CEO of Citizens, says as many as 300,000 policies could be removed under the new loan program—possibly by the start of 2013. If so, the assessment risk over the heads of nearly all Florida policyholders would be reduced $1.2 billion (for a 1-in-100 year event), he adds.

Citizens says it would need to pay the private reinsurance market $240 million per year to reduce the same amount of probable maximum loss.

A loan of up to $50 million per insurer is being made available in order to entice the private property insurance market to take Citizens' policies for up to 10 years.

Many of Citizens' policies are significantly underpriced and any insurer willing to participate in this take-out proposal cannot increase rates on any assumed policy at renewal by more than 10 percent. The loans are meant to make it easier for a private insurer to take the underpriced risk.

The plan was developed after asking for proposals from the private market, says Samuel Miller, executive vice president of the Florida Insurance Council, a trade group that has not taken a formal position on the surplus notes plan.

But, he says, "Any proposal that would reduce Citizens' exposure should be considered, and this is a legitimate proposal. A majority of Citizens' policies are underpriced, making it difficult for a private insurer to take them. This is designed to make it work."

Some FIC-member companies may be interested in assuming some Citizens' policies under the loan program.

This new depopulation plan is separate from an announcement made by Insurance Commissioner Kevin McCarty the same day Citizens' Depopulation Committee met to go over its latest depopulation idea. He approved four domestic insurers to remove a total of 150,000 policies from the state's bloated last-resort insurer on Nov. 6 under the old program with no financial incentives.

It remains unclear who will make sure no one insurer takes out too much risk in relation to the loan it receives from Citizens. The OIR says it couldn't say until it "had a chance to evaluate [the proposal] in its final form." The OIR must review and approve the plan.

In his statement, McCarty says four additional companies expressed interest in removing about 181,000 additional policies from Citizens' books contingent on the surplus notes program being approved.

McCarty sent a letter to Citizens, urging the insurer to give priority to insurers that have been approved to take-out policies without financial incentives.

The proposal has its critics. Some lawmakers object to transferring surplus to the private market. And there remains some concern about the fact policyholders can still opt-out and chose to stay with Citizens at the point of first notice and they can go back to the state-run insurer at renewal.

The 300,000 policy-count prediction may be lofty. Many insurers will be gunning for a lot of the same, less-risky policies.

But Jeff Grady, president and CEO of the Florida Association of Insurance Agents, says any plan that would result in less reliance on Citizens would be alike "living a fantasy."

"I think [Citizens] spent a lot of time on this and did some good analysis," he says. "It looks pretty reasonable. It's lending money. It's not giving it away."

With policies potentially staying off Citizens' books for a decade, Grady could not be happier.

"I'm not discounting that take-outs are hard, but agents will own that business again," he says.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking insurance news and analysis, on-site and via our newsletters and custom alerts

- Weekly Insurance Speak podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical converage of the employee benefits and financial advisory markets on our other ALM sites, BenefitsPRO and ThinkAdvisor

Already have an account? Sign In Now

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.