NU Online News Service, Feb. 29, 3:58 p.m. EST

Faced with the daunting task of improving margins in an economically strained environment, insurers are finding ways to increase efficiency, and many see policy administration as an area where technology can accomplish that goal, according to a recent report.

This week, the consulting firm Capgemini and Efma (European Financial Marketing Association), a bank and insurance industry association, both based in Paris, released their World Insurance Report 2012. The report says that as investment income has declined, the property and casualty insurance industry is "forced to concentrate on improving the building blocks of underwriting performance: claims, and operational and acquisition ratios."

As a result, the industry is seeking to improve the efficiency of processing claims, operations and distribution of insurance to lower costs and enhance profitability.

In a survey of 71 insurance executives covering 17 insurance markets that include the United States, Europe and Asia, the report says that most of the world's P&C insurers have "experienced gains in profitability" over the past two years as they have seen some recovering in investment income after the financial crisis of 2008. However, the continued weak economy has taught them that they cannot rely on investment income alone to shore up profitability.

In a survey of 71 insurance executives covering 17 insurance markets that include the United States, Europe and Asia, the report says that most of the world's P&C insurers have "experienced gains in profitability" over the past two years as they have seen some recovering in investment income after the financial crisis of 2008. However, the continued weak economy has taught them that they cannot rely on investment income alone to shore up profitability.

Raising prices in not an answer because the competitive insurance marketplace means customers can easily turn elsewhere when it is a question of price, the report notes.

Pursuing greater efficiency in underwriting performance by minimizing their "claims, acquisition [acquiring customers] and other operational costs" while continuing to grow their business is an increasing focus of carriers.

One major area of improvement is policy administration, which insurers consider to be the next priority to achieving "cost and operation efficiency." Insurers are increasingly turning to information-technology solutions to achieve that goal.

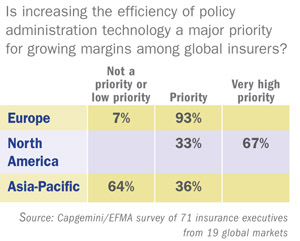

In the survey, over the next two years, 93 percent of insurance executives in Europe say that policy administration improvements, or transformation, is a priority for them, with 67 percent saying it is a very high priority.

In North America, 67 percent of executives called it a very high priority, while 33 percent did not consider it a priority.

For Asia-Pacific carriers, the number drops to 36 percent, with 9 percent saying it is a very high priority.

The survey points out that a major reason for the lower concern in the Asia-Pacific region has to do with the relative newness of insurance in that region that allowed them to incorporate newer technology.

One of the major issues for Europe and North America carriers is that they are still working with inefficient legacy systems. This affects rolling out new products and inhibits their ability to "compete in a customer-centric market."

The report says that transforming their policy administration system carriers would reduce their operational costs by reducing cost per policy by 30 percent. They would also reduce business and technology process inefficiency by 30 percent.

"By transforming these systems, insurers can better manage current market challenges including regulatory-compliance issues, customers and intermediary satisfaction, aging and inflexible systems, and protracted product launches by increasing the speed to market by up to 60 percent.

Keith Gage, vice president, Capgemini Financial Services, told National Underwriter that for the first time in a decade when it comes to upgrading policy-administration technology, there are off-the-shelf solutions and the tools available for insurers to build the system from scratch. Dealing with the legacy-issue questions, he says these systems can "go right after the constraints" that have kept insurers "in a straightjacket" from achieving efficiencies.

With those efficiencies, he says carriers have seen where the roll out of a new product that once to nine months can then take a couple of weeks.

"It gives them a lot more agility and the ability to move faster to introduce product, deal with regulatory issues and make rate changes," says Gage.

What is often holding back insurers is the time and cost to make the changes, he says. It is not unusual for a changeover to take three to five years, and could cost in excess of $30 million, but that all depends on the size of the carrier, using $30 million as a benchmark figure, he notes.

However, making the changes can have substantial impact on an insurer's bottom line, both producing efficiencies that save money and in allowing the carrier to grow market share with their customers and improve the delivery of the product to both insurance agents and the customer.

"It is one of the few areas where a carrier can get cost benefit and gain customers," says Gage.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking insurance news and analysis, on-site and via our newsletters and custom alerts

- Weekly Insurance Speak podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical converage of the employee benefits and financial advisory markets on our other ALM sites, BenefitsPRO and ThinkAdvisor

Already have an account? Sign In Now

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.