In our annual “State of the Line” study, the National Council on Compensation Insurance Inc. (NCCI) delivers a comprehensive report analyzing the entire workers' compensation market—from the implications of the overall economic environment, to current and expected industry conditions, to political considerations and more.

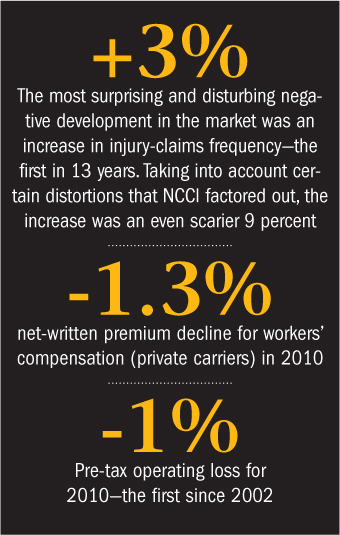

Unfortunately, our analysis this year shows that conditions in the workers' comp industry continue to deteriorate. The line continues to experience an ever-lengthening list of challenges, including poor underwriting results, declining (albeit more slowly) premiums, an uptick in claim frequency, and an uncertain regulatory and inflationary climate.

Unfortunately, our analysis this year shows that conditions in the workers' comp industry continue to deteriorate. The line continues to experience an ever-lengthening list of challenges, including poor underwriting results, declining (albeit more slowly) premiums, an uptick in claim frequency, and an uncertain regulatory and inflationary climate.

Let's broadly examine these negative forces and the overall market condition.

Recommended For You

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking insurance news and analysis, on-site and via our newsletters and custom alerts

- Weekly Insurance Speak podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical converage of the employee benefits and financial advisory markets on our other ALM sites, BenefitsPRO and ThinkAdvisor

Already have an account? Sign In Now

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.