While captive-insurance experts contend that the market is healthy, with solid formations, they also note a variety of concerns, including Solvency II, the Dodd-Frank Act and fraud.

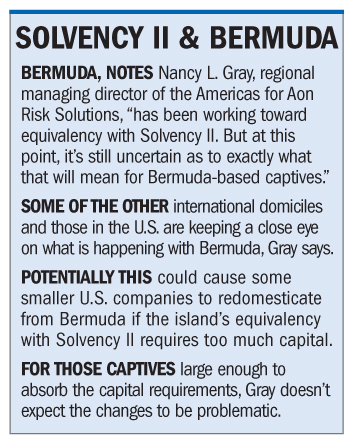

For example, Solvency II creates more capital requirements and governance standards, making it “onerous” for owners of captives domiciled in Europe, says Nancy L. Gray, regional managing director of the Americas for Aon Risk Solutions.

While this won't directly impact U.S.-domiciled captives, there are possible domestic ramifications “from the standpoint that you have a lot of U.S. parents that own a captive in [Europe] and are being faced with Solvency II implications,” Gray adds.

While this won't directly impact U.S.-domiciled captives, there are possible domestic ramifications “from the standpoint that you have a lot of U.S. parents that own a captive in [Europe] and are being faced with Solvency II implications,” Gray adds.

Recommended For You

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking insurance news and analysis, on-site and via our newsletters and custom alerts

- Weekly Insurance Speak podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical converage of the employee benefits and financial advisory markets on our other ALM sites, BenefitsPRO and ThinkAdvisor

Already have an account? Sign In Now

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.