The CEO of Fortegra Financial believes he has a distinct edge as he competes to acquire property and casualty wholesale brokerages and regional specialty agencies to add to his firm's suite of insurance-service operations.

What is the advantage? Being a New York Stock Exchange-listed public company.

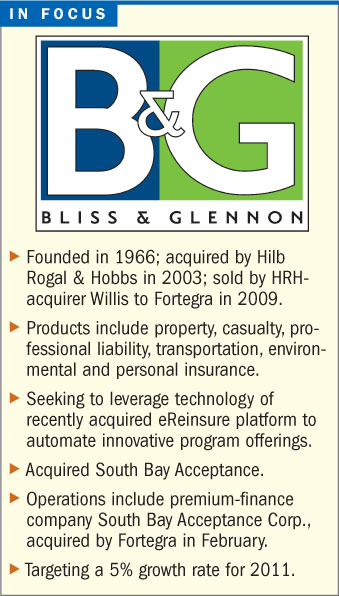

“We think the public-company [status] is critical to rewarding the brokers who make your business happen,” says Richard Kahlbaugh, who heads a group that includes credit-insurance operations, a business-process-outsourcing (BPO) platform, and Redondo Beach, Calif.-based wholesaler Bliss & Glennon (B&G).

“We think the public-company [status] is critical to rewarding the brokers who make your business happen,” says Richard Kahlbaugh, who heads a group that includes credit-insurance operations, a business-process-outsourcing (BPO) platform, and Redondo Beach, Calif.-based wholesaler Bliss & Glennon (B&G).

Recommended For You

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking insurance news and analysis, on-site and via our newsletters and custom alerts

- Weekly Insurance Speak podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical converage of the employee benefits and financial advisory markets on our other ALM sites, BenefitsPRO and ThinkAdvisor

Already have an account? Sign In Now

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.