The continuing soft market is weakening the credit quality of property and casualty insurers, making their future “problematic,” with no turnaround in sight, according to an analysis by Moody's Rating Service.

In its weekly credit outlook report, Moody's noted that the latest Council of Insurance Agents and Brokers price trend survey (http://bit.ly/dpjuRw) underscores the continuing soft market hammering industry top- and bottom lines.

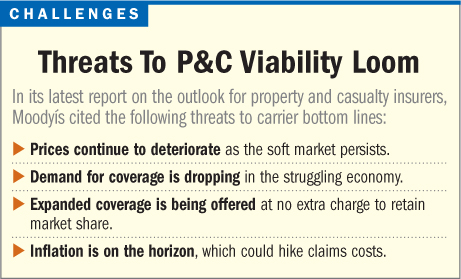

Average premium rate declines since the third quarter of last year stand in excess of 5 percent. During the second quarter of this year, insurance brokers surveyed said rate declines averaged more than 6 percent.

“In the absence of a significant catastrophe, we do not expect a reversal in the downward slide of commercial property pricing in the near future,” Moody's said, regarding the property side of the business, while noting that on the casualty side, business reflects the same continued downward slide.

“In the absence of a significant catastrophe, we do not expect a reversal in the downward slide of commercial property pricing in the near future,” Moody's said, regarding the property side of the business, while noting that on the casualty side, business reflects the same continued downward slide.

The only reason insurer earnings have not generally reflected the soft market's impact is that carriers tapped reserves built up during the favorable development period from 2003 through 2006, when rates “were at peak levels,” Moody's explained.

However, moving forward, earnings on casualty business in 2011 and beyond will “cease to benefit from favorable legacy reserve development,” according to Moody's, which warned that those p&c insurers that have written underpriced business will start to see bottom-line losses that will have “an impact to capital in more severe cases.”

Results from the CIAB survey indicate carriers are also offering broader terms and conditions without any corresponding price hike in order to keep market share. This practice, Moody's said, could have long-term negative impact and is “potentially more problematic than rate inadequacy,” because it is difficult to understand the full impact such changes can have on a company due to “reduced transparency.”

“We believe the sector is offering greater capacity than demand can absorb, and the medium-term outlook doesn't look promising” given the decline in insurance coverage demand due to the economic downturn.

Finally, inflation is another concern for the industry, according to Moody's, which warned that insurer profitability could take a hit from the “unexpected cost inflation” to claims impacted by wages, medical costs and commodity prices.

Pano Karambelas, vice president and senior credit officer for Moody's, told National Underwriter that “no one knows how long this is going to take” before the soft market sees a turnaround in pricing, limits, terms and conditions.

Want to continue reading?

Become a Free PropertyCasualty360 Digital Reader

Your access to unlimited PropertyCasualty360 content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Breaking insurance news and analysis, on-site and via our newsletters and custom alerts

- Weekly Insurance Speak podcast featuring exclusive interviews with industry leaders

- Educational webcasts, white papers, and ebooks from industry thought leaders

- Critical converage of the employee benefits and financial advisory markets on our other ALM sites, BenefitsPRO and ThinkAdvisor

Already have an account? Sign In Now

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.